%20vs.%20California%20(1848%E2%80%931898)%20thumbnail.avif)

Eloro Resources (TSX: ELO), a company focused on the exploration and development of mineral properties, continues to advance its flagship asset in South America. Since our last discussion in September 2025, Eloro has further delineated its Iska Iska property in the Bolivian tin belt. The company recently released an updated Mineral Resource Estimate, expanding the project's scale to over 1 billion tonnes of combined Indicated and Inferred polymetallic mineralization, while also noting increased silver grades and improved tin recoveries.

latest articles

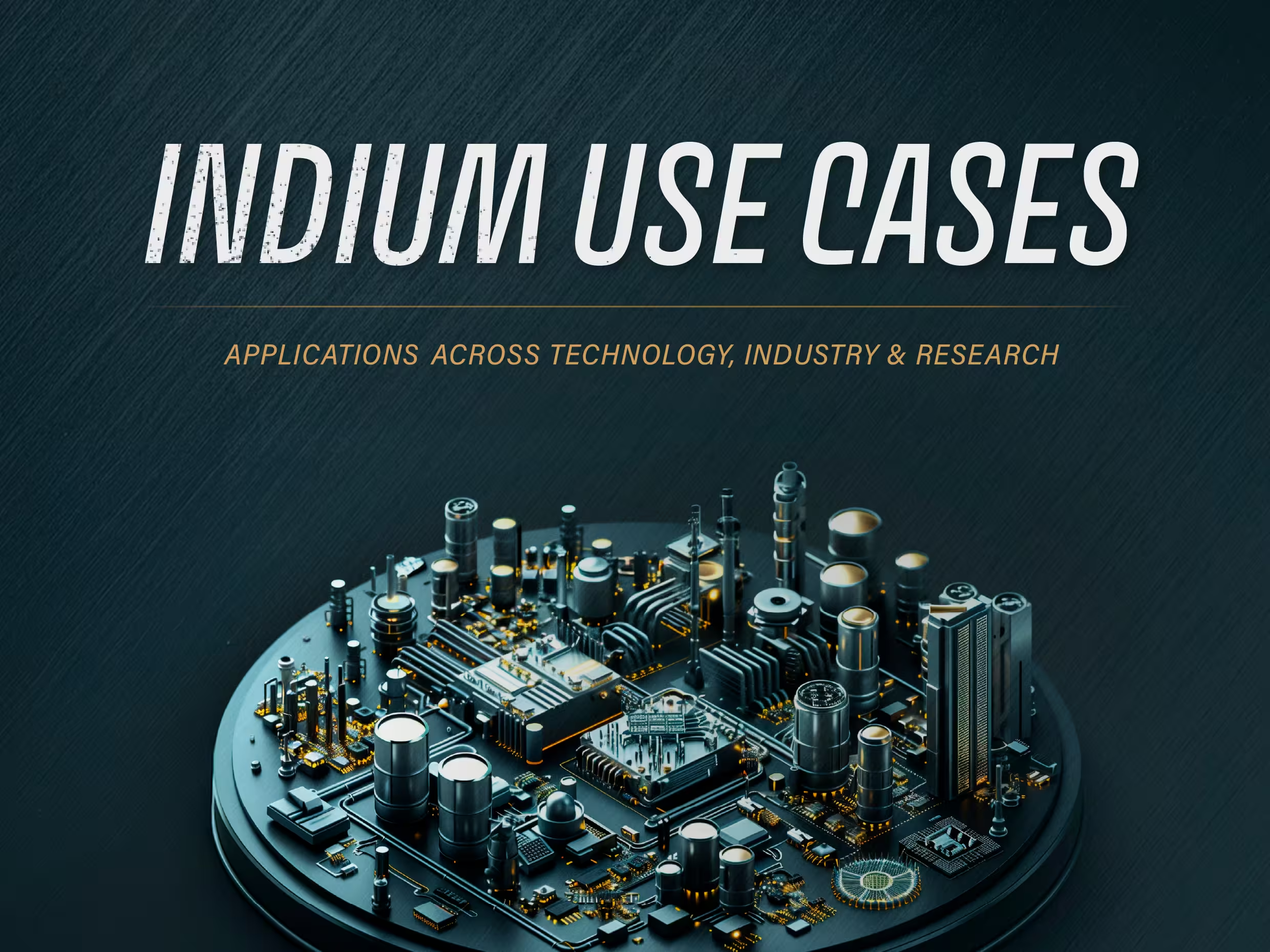

Where Indium Goes: The Metal Behind Screens, Chips, and Solar

Where Indium Goes: The Metal Behind Screens, Chips, and Solar

Indium is one of the metals you never see but use constantly. As indium tin oxide, it forms the transparent conductive coating on nearly every LCD and touchscreen, and that single application still accounts for most global consumption, according to the USGS. But the metal's role is broadening. Its compounds now sit inside the high-speed optical chips that route data through AI data centers, a shift that has turned a quiet, display-driven material into one buyers watch closely, especially as China refines about 70% of it and has begun tightening the flow.

popular

highlights

View All

The Uranium Opportunity: Limited Supply Meets Rising Demand

The Uranium Opportunity: Limited Supply Meets Rising Demand

In 2025, global uranium mine supply is projected to be 176 million pounds, while demand is expected to reach 182 million, resulting in a 6 million-pound deficit. This shortfall is expected to increase significantly over the next 15 years. By 2040, uranium demand is forecast to surge to 397 million pounds, a staggering 118% increase from 2025 levels, while supply is only expected to grow modestly to 201 million, up just 14%. The result: an anticipated deficit of 197 million pounds, equivalent to the output of 11 Cigar Lake Mines, one of the world’s largest uranium producers.

Gold

View All

Gold Production 2025

Gold Production 2025

While 2025 will be remembered for gold's historic price rally, setting 53 all-time highs and averaging a record $3,431 per ounce, the industry's physical output told a different story. According to the World Gold Council, global mine production grew by a mere 1% year-over-year to reach 3,672 tonnes. This muted supply response illustrates the rigid realities of modern mining: even when prices skyrocket, extracting more metal from the ground remains a slow, highly regulated, and capital-intensive process.

The World’s Top 10 Largest Gold Mines by Production (2025)

The World’s Top 10 Largest Gold Mines by Production (2025)

Historically, gold has maintained a steadfast reputation as a safe-haven asset, with investment demand spiking significantly during times of heightened economic uncertainty and recession. As global markets continue to navigate complex macroeconomic pressures in 2026, the origin of the world's physical gold supply remains a critical focal point for investors and industry professionals alike.

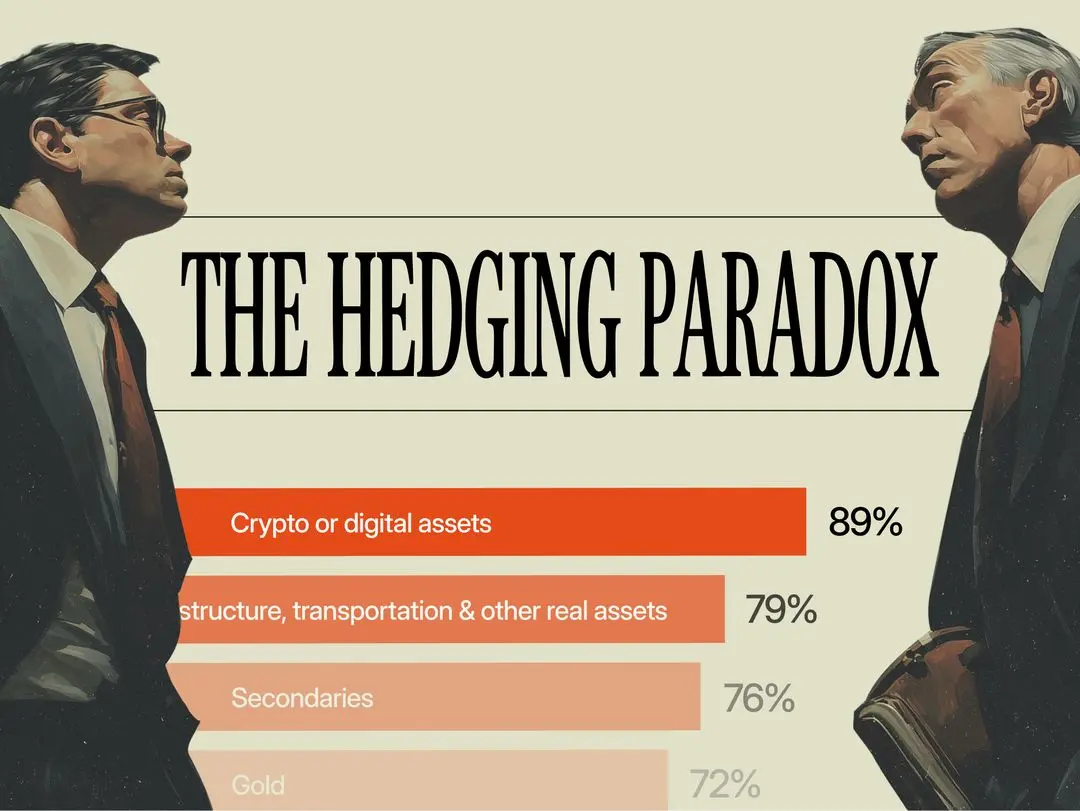

The Hedging Paradox: Why the World's Wealthiest Families Are Ignoring Real Assets

The Hedging Paradox: Why the World's Wealthiest Families Are Ignoring Real Assets

The geopolitical temperature is boiling. Between shifting global alliances, fractured supply chains, and persistent structural inflation, macro uncertainty is the defining feature of 2026.

silver

View All

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

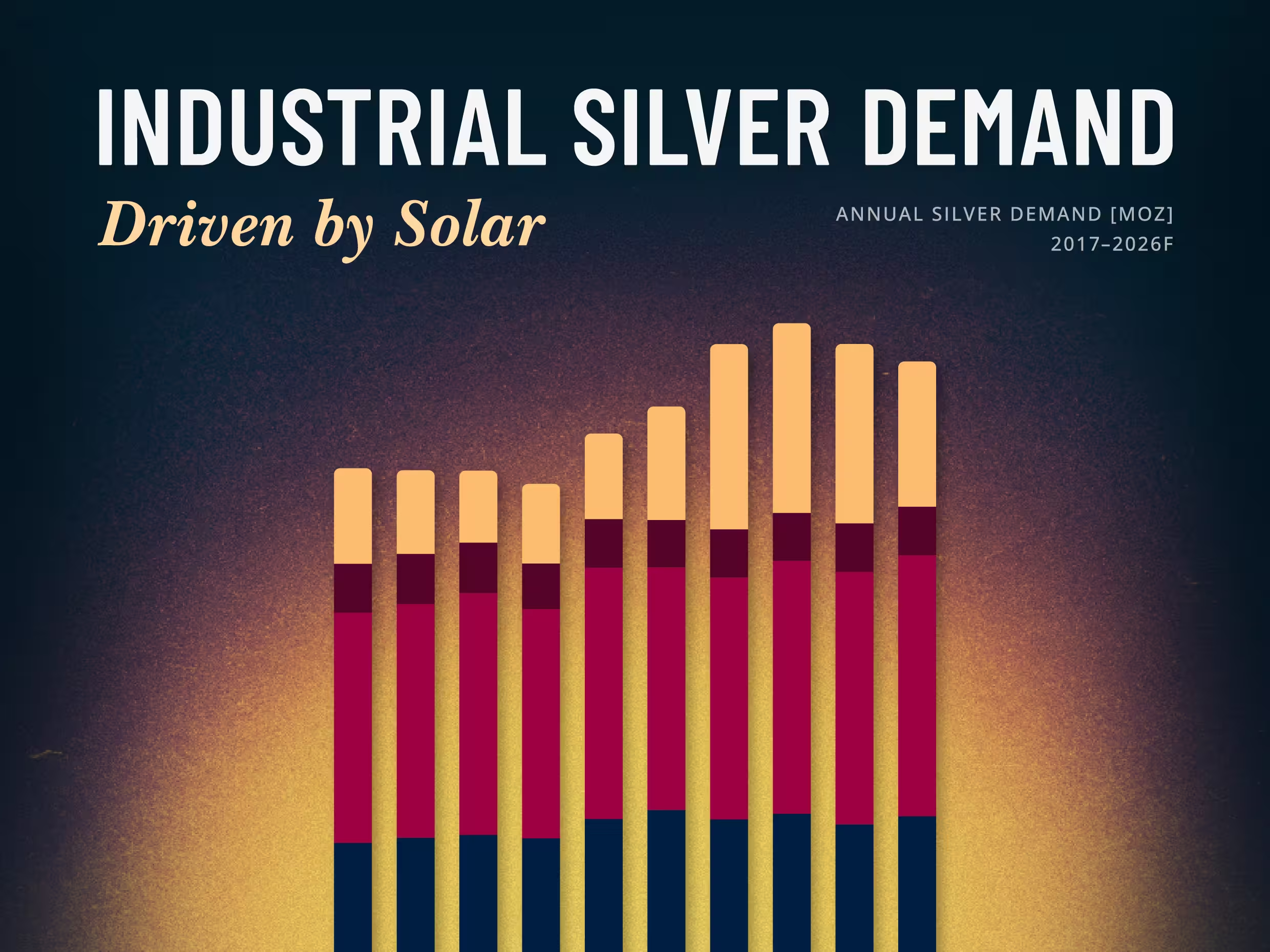

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.

copper

View All

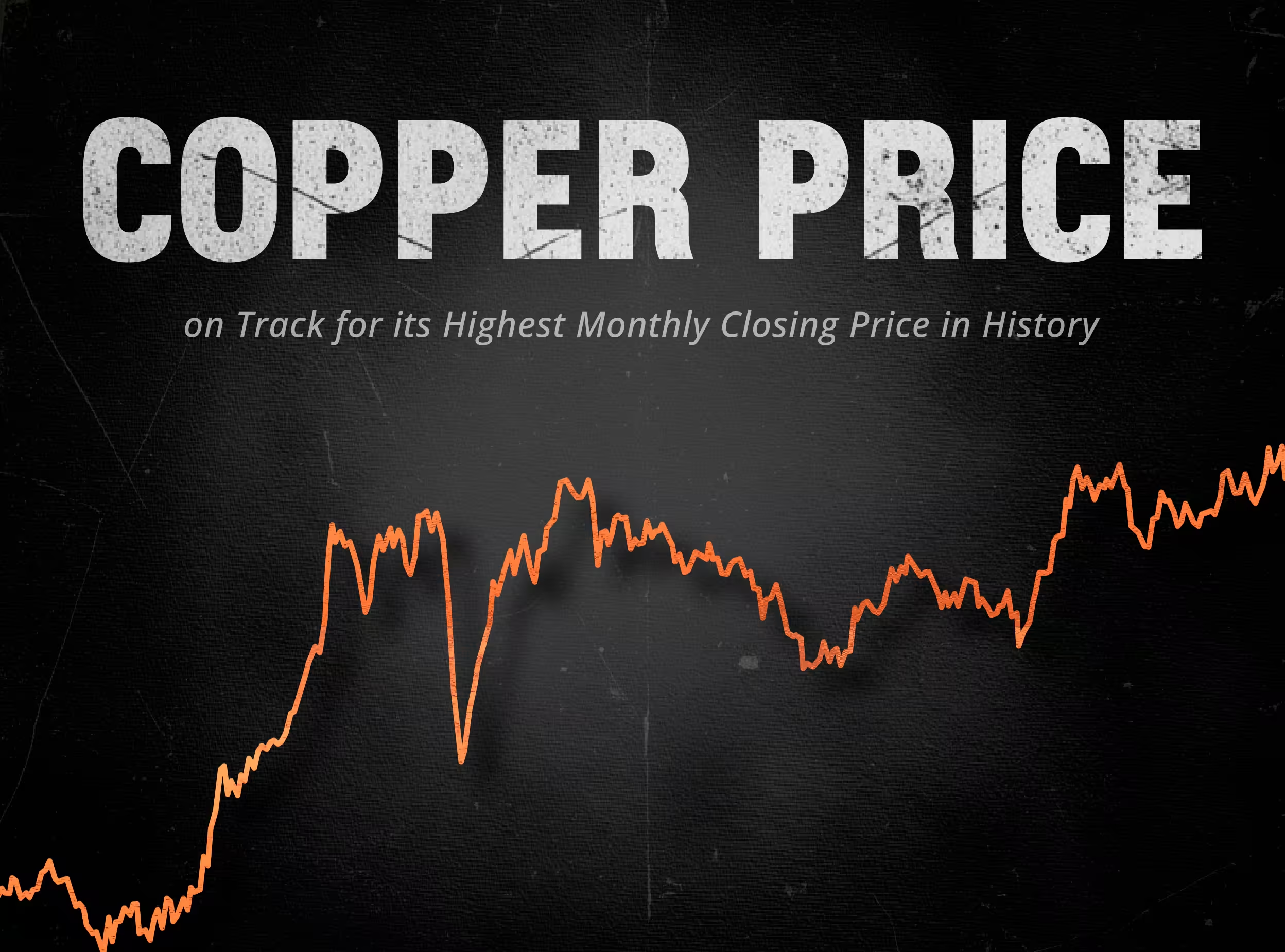

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.

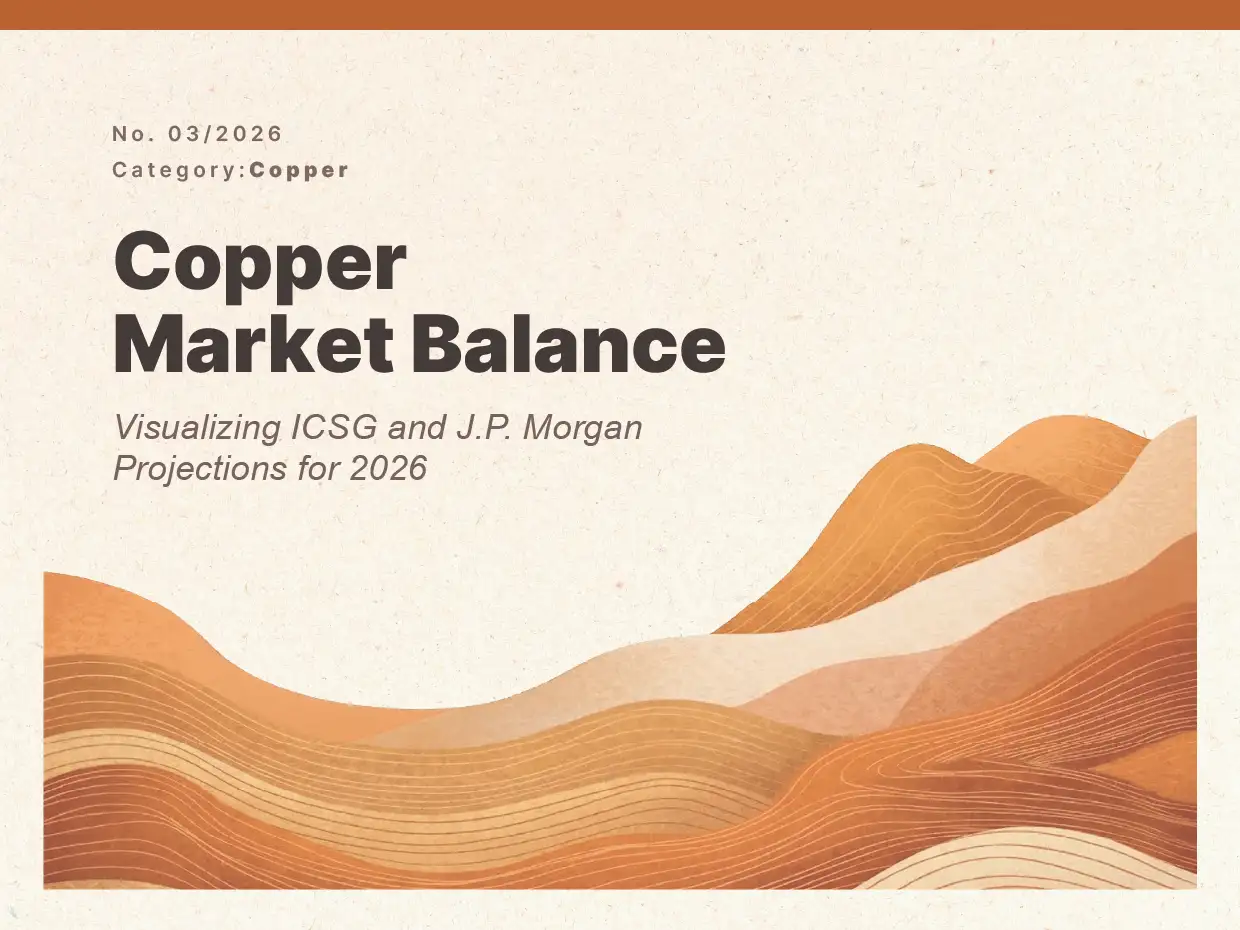

Copper Market Balance: A Look at 2026 Deficit Forecasts

Copper Market Balance: A Look at 2026 Deficit Forecasts

For years, analysts modeling the global copper market were comforted by a reliable buffer of surplus supply. But as our latest data visualization reveals, that cushion has violently evaporated. The International Copper Study Group (ICSG) has officially abandoned its projected surplus for 2025 to officially forecast a 150,000-metric-ton deficit for 2026—the market's first structural shortage since 2009. Wall Street is bracing for an even harsher reality.

commodities

View All

Rare Earths and the F-35: The Defense Supply-Chain Bottleneck Behind America's Most Advanced Fighter Jet

Rare Earths and the F-35: The Defense Supply-Chain Bottleneck Behind America's Most Advanced Fighter Jet

In September 2022, the Pentagon quietly stopped taking delivery of new F-35 fighter jets. The reason was not a design flaw or a manufacturing defect. A single small magnet inside the plane's engine had been made using an alloy from China, which is banned under U.S. defense procurement law.

Apple Outweighs Every Listed Miner on Earth, and It Is Not Even the Biggest Company

Apple Outweighs Every Listed Miner on Earth, and It Is Not Even the Biggest Company

One consumer-electronics company is now worth more than every publicly traded mining company on Earth combined. The graphic above captures the June 5 snapshot, when the 317 publicly traded miners tracked by CompaniesMarketCap were worth about $3.48 trillion

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

For 24 years SpaceX stayed private. Then, on June 12, 2026, it began trading on the Nasdaq in the largest IPO in history, priced at a $1.77 trillion valuation. Barely three weeks later the rocket and satellite maker is worth even more. As of early July, SpaceX carried a market capitalization of about $2.1 trillion, the seventh-highest of any public company on Earth, and it joins the Nasdaq-100 on July 7

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

We've covered zinc's role in energy, health, and sustainability before, alongside the supply base concentrated in a handful of mega-mines and the production map that has shifted toward Asia since the mid-1990s. The story of 2025 is what changed on the demand side. In November, the U.S. Geological Survey retained zinc on its final 2025 List of Critical Minerals.

Interviews

View All

Subscribe to our newsletter

Get the latest news and insights delivered directly to your inbox.